“I pay tax on my drawings, right?”

“I don’t have to pay any tax because I’ve only taken drawings”

“Isn’t drawings the same as a salary?”

Drawings is one of the most confusing areas for business owners and it’s not surprising. Google “What are drawings” and you’ll find a huge range of answers using a bunch of technical words. It’s almost guaranteed to give you a migraine.

If you not entirely sure about drawings or other accountanty terms like shareholder current accounts and shareholder salaries, you’re not alone. So we’ve broken it down and then pulled it back together in a scenario so you can finally get your head around drawings.

Your drawings are not your income

Drawings is simply money that you have borrowed (with-drawn) from the company. You don't actually get any income from the company until the end of the year, when together we make a decision about how much you should be paid for the year.

This is based on:

- how much profit the company has made

- how involved each shareholder has been in working in the business,

- how much you’ve taken in drawings during the year, and

- what’s the most tax effective way of allocating that profit.

The income you are allocated from the company at the end of the year is known as a shareholder salary. Just like wages paid to an employee, the shareholder salary is treated as an expense which reduces the net profit of the company.

The difference between the wages you pay employees and a shareholder salary is that wages are paid at least monthly and have PAYE taken out. A shareholder salary is allocated at the end of the year and you still have to pay the income tax.

Because you only get your shareholder salary at the end of the year, another way of thinking about drawings is like an advance on your salary.

Drawings and your shareholder salary are recorded in your Shareholder Current Account – which is another mystical accounting concept we'll expore next.

Your Shareholder Current Account is a loan between you and your company

It can be helpful to think of your shareholder current account like a bank account with your company being ‘the bank’.

When you take drawings, you are borrowing money from the company. When you put money into the business you are making a cash deposit into the company. Your shareholder current account also gets topped up when the company allocates you a shareholder salary.

If your shareholder current account is in credit, then the company owes you the money. You can withdraw that at any time as long as the company has cash in it’s actual bank account to pay you.

If your shareholder current account is overdrawn it means you owe the company money. And just like the bank, the company will charge you interest on your overdrawn current account.

Lets tie this all together using a scenario

- Sarah and Dave are the directors and shareholders of The Cakery Ltd, a specialist cake business.

- Sarah works in the business, while Dave is a builder working for a large construction company.

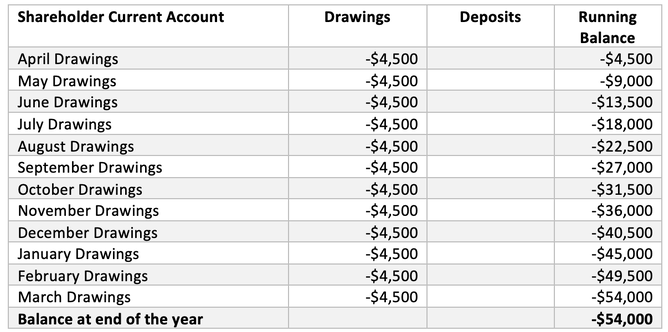

- During the year Sarah takes $4,500 each month as drawings from her company

- At the end of the year, her total drawings were $54,000

- The Cakery Ltd has made a profit of $71,000 for the year

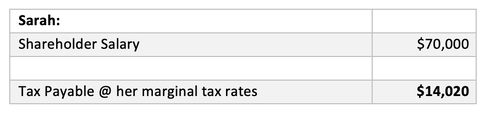

- After reviewing the profit, who worked in the business and the most tax effective way to allocate profit, we recommend that Sarah receive a shareholder salary of $70,000 for all her hard work.

- Dave does not get paid anything as he doesn’t work in the business.

Drawings, Shareholder Salaries and Shareholder Current Accounts

Throughout the year, Sarah has taken $4,500 each month in drawings. Each month Sarah’s shareholder current account becomes more overdrawn as she takes drawings in advance of the salary she expects to get at the end of the year.

Although her shareholder current account is overdrawn, Sarah knows that at the end of the year the company will allocate the profits to her as a shareholder salary.

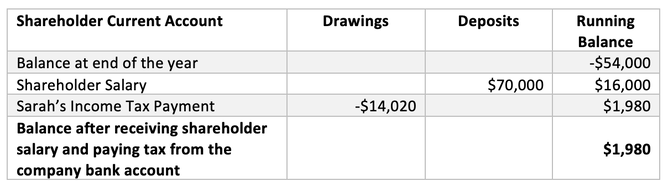

After making a profit of $71,000, The Cakery Ltd pays Sarah a shareholder salary of $70,000. But because she had already taken drawings as an advance on some of her salary Sarah doesn’t actually receive the shareholder salary in cash.

Instead, the $70,000 shareholder salary is used to top up her current account and puts her back into credit.

How much tax needs to be paid & who pays it?

As the company has decided to allocate Sarah a shareholder salary of $70,000, it's net profit is reduced to $1,000. The Cakery Ltd will pay tax on it’s net profit of $1,000 at the company tax rate of 28%.

Sarah has to pay tax on her Shareholder Salary, along with any other income she might have from interest, dividends, rental properties, or other jobs.

As the only income Sarah received is from her shareholder salary, her tax is calculated on a total income of $70,000. She will pay tax on this at her marginal tax rates, which works out to $14,020.

Sarah now has to find $14,020 to pay her tax. Fortunately, her drawings were less than her shareholder salary and she has a balance of $16,000 in her shareholder current account that she could still take out of the company.

Sarah decides to have the company pay her income tax of $14,020 on her behalf. This is also a type of drawings, and leave her with a balance of $1,980 owed to her.

Key Takeaways

- Drawings is money you borrow from the company

- A shareholder's salary is your share of the company's profits for work you do in the business

- You pay tax on your shareholders salary

- The company pays tax on it's net profit after it's paid you a shareholder salary

- A Shareholders Current Account is a loan between you and the company.

What next?

At Trio, we make sure to breakdown accounting jargon and technical tax stuff so that you can feel confident around your numbers and understand the essentials when it comes to business finances and tax.

If you're new to business or would like more support, book a discovery call with us and find out how we can help.